State space models, a brief introduction

State space models (sometimes known as latent variable models) are equivalent to HMMs

Assumptions:

markovian property

zero mean, iid Gaussian noise:

Additionally, we just consider stationary models, that is, parameters of are considered constant in time.

Applications:

Object tracking

Process modeling

Optimization

System identification and modeling

Forecasting

Exponential smoothing

ARMA / Box Jenkins

ARIMAX

All these applications have developed slightly different notations and consider slightly different terms and assumptions.

We will review them under a general framework / notation, from which all of them can be derived.

Linear, time invariant models

We will restrict the explanation to linear models, but all the explained properties hold also for non-linear models.

Moreover, we will assume that the parameters of the model are fixed in time.

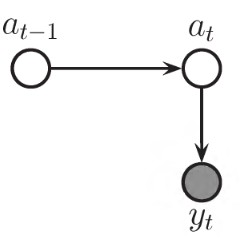

Process form - Multiple source of errors

→ Kalman filter gain K →

Innovation form - Single source of error

All the tractation of exponential models for forecasting assumes an innovation form. We briefly review the Kalman filter theory which must be used to pass from process to innovation form.

Kalman filter

The Kalman filter is one of the most important and common estimation algorithms. It performs an exact Bayesian filtering for linear-Gaussian state space models. It can be used to:

estimate hidden (unknown) states based on a series of (noisy) measurements. Ex: GPS location and velocity = hidden states, differential time of the satellites' signals' arrival = measurements. Ex2: trajectory estimation for the Apollo program.

predict / forecast future system’s state based on past estimations. Ex: nowcasting

Example: tracking positions

Suppose we want to track the position of a robot in the woods, having just the readings of a unreliable GPS tracker.

We can write a useful state space model for the tracking using our knowledge on the laws of motion:

…write the balance equations in matrix form

…and obtain the stochastic formulation

Uncertainty propagation for linear-Gaussian variables

The zero-mean Gaussian distribution is completely determined by its covariance matrix

If the variable has a Gaussian distribution , so it has its linear transformation. You can view the linear operator as a superposition of two linear transformations: one on the mean value of , which can be treated as deterministic, and one on an associated zero-mean error distributed as :

Why is the covariance of the Gaussian rescaled in this way? From the definition of covariance:

Uncertainty propagation

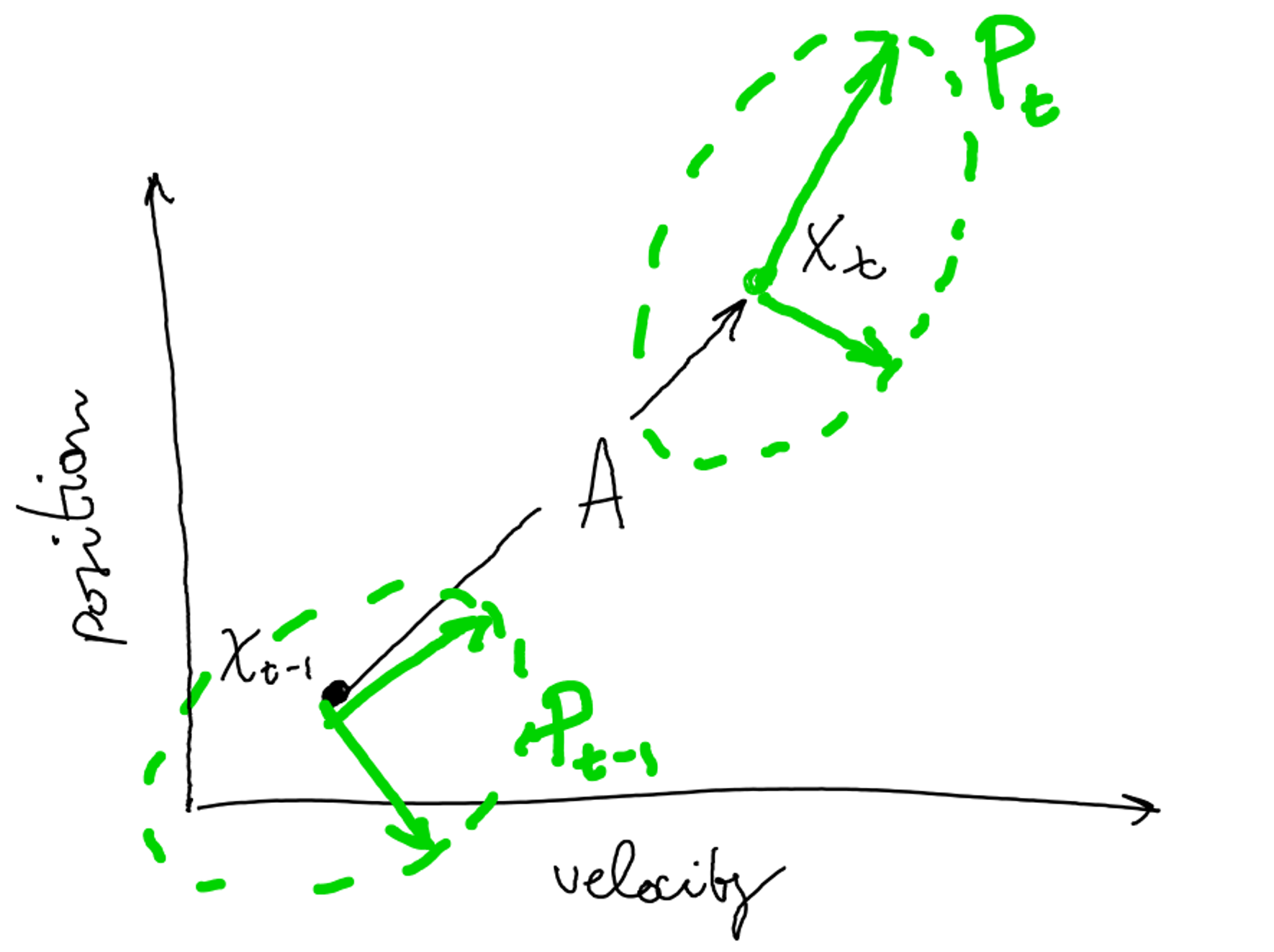

In general, to improve the state estimation, it is useful to know if states are correlated. In this case, the robot could have higher velocities at particular positions (e.g. on a slope). Let’s assume the states have a Gaussian distribution where is the (symmetric) states’ covariance matrix.

How the state’s uncertainty spreads through time?

Deterministic step: shift

State uncertainty prediction for next step t, given the state covariance at time t-1

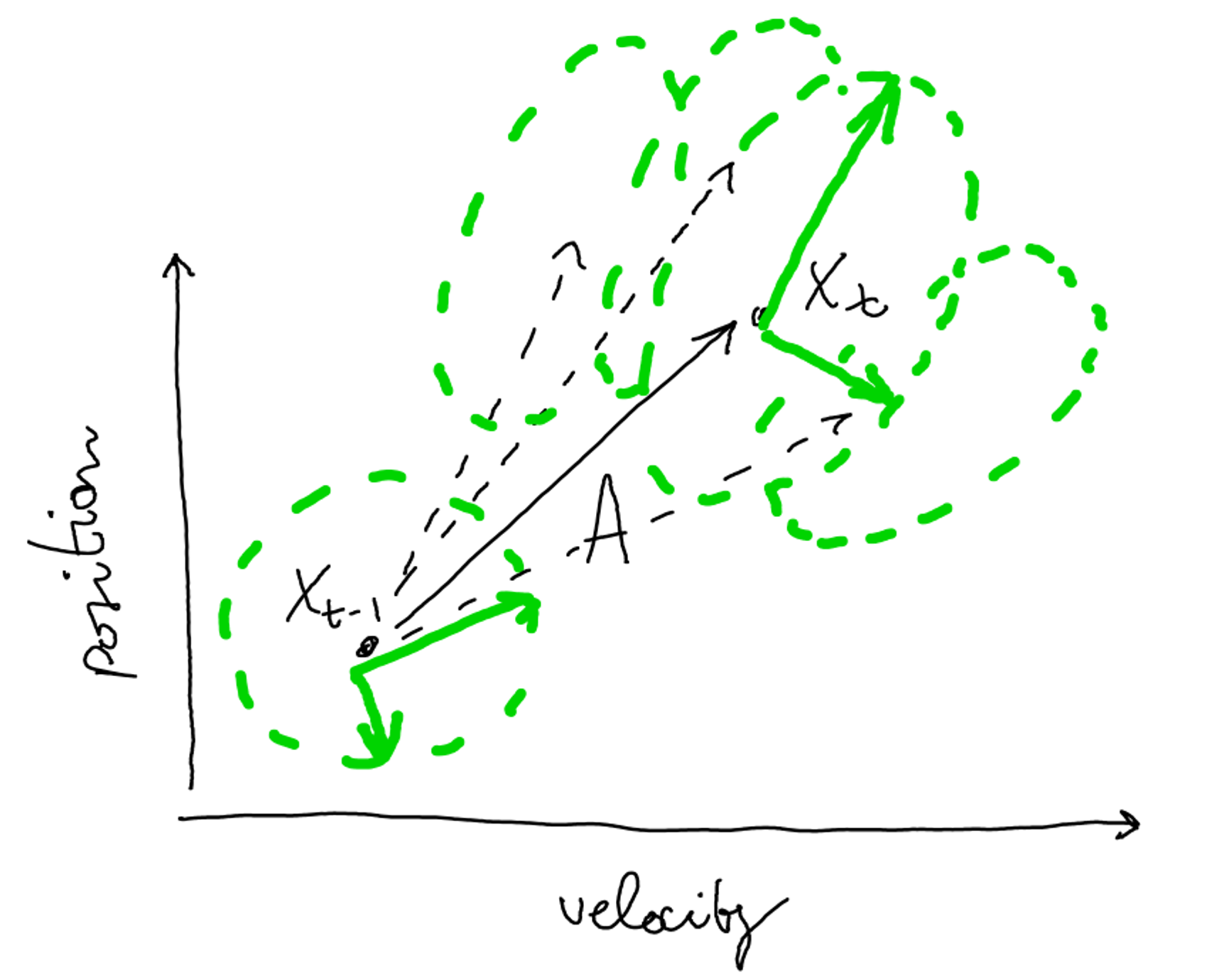

System noise: Gaussian blob→ still Gaussian

Additional uncertainty given by the system noise, affecting the next state’s prediction

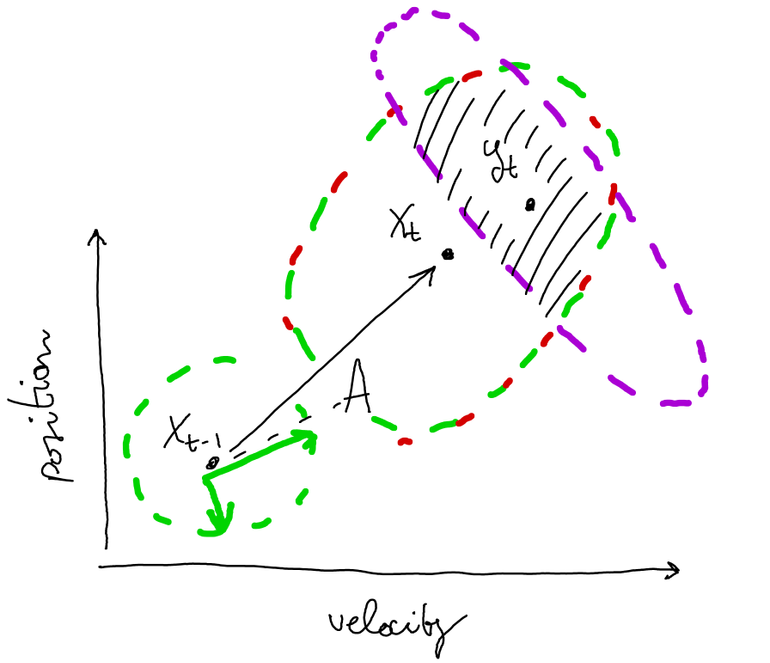

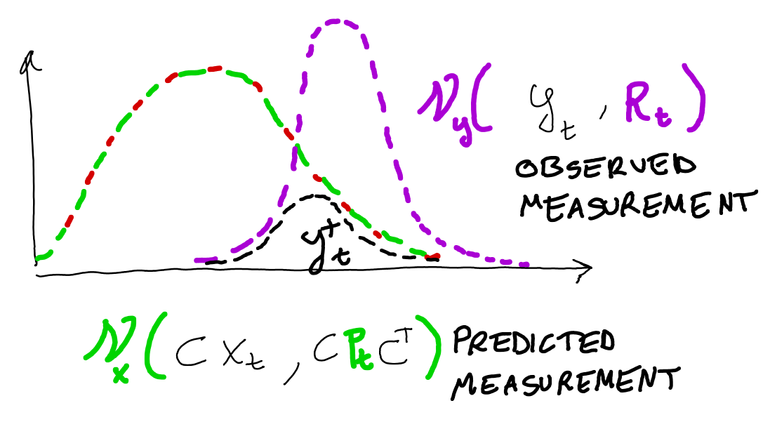

Exploit sensor’s observations:

predicted measurement

observed measurement

The uncertainty on the prediction can be reduced when we observe a new output from the GPS

Derivation of Kalman gain

The dashed space in the last picture shows the region where is most probable to find the state at time t, given the observations from the sensor. How does the predicted and observed measurements combine? Since we said that :

The multiplication of two univariate gaussians leads to:

We can then write

Interpretation: we are linearly correcting the measurement with the sensor’s values, with a weight proportional to the uncertainty on the predicted measure.

The covariance update can be written as:

Linear state space model estimation

How can we estimate A, B, C, D, if we don’t observe state x?

How can we estimate A, B, C, D, if we don’t observe state x?Noise elimination

Since in the innovation form the noise enters both the equations at time t, we can eliminate one equation by substituting back in the first equation:

State elimination

We can now recursively find the state at the next step as an expression of previous inputs and observations:

start with

explicit next state as

repeat iteratively

By recursive substitution, we get:

We can see that at each step , the new state is a function of the initial state and a weighted sum of past inputs and observations .

If we now use the state at time as input to predict the new observation , we get:

This means that the forecasts of a state-space model in innovation form can be reformulated as a weighted sum of past observations and inputs. This form is also called the reduced form of the model.

This form show that ARIMA models can be formulated as SS models. Also exponential smoothing models can be formulated as SS, as we see in the following

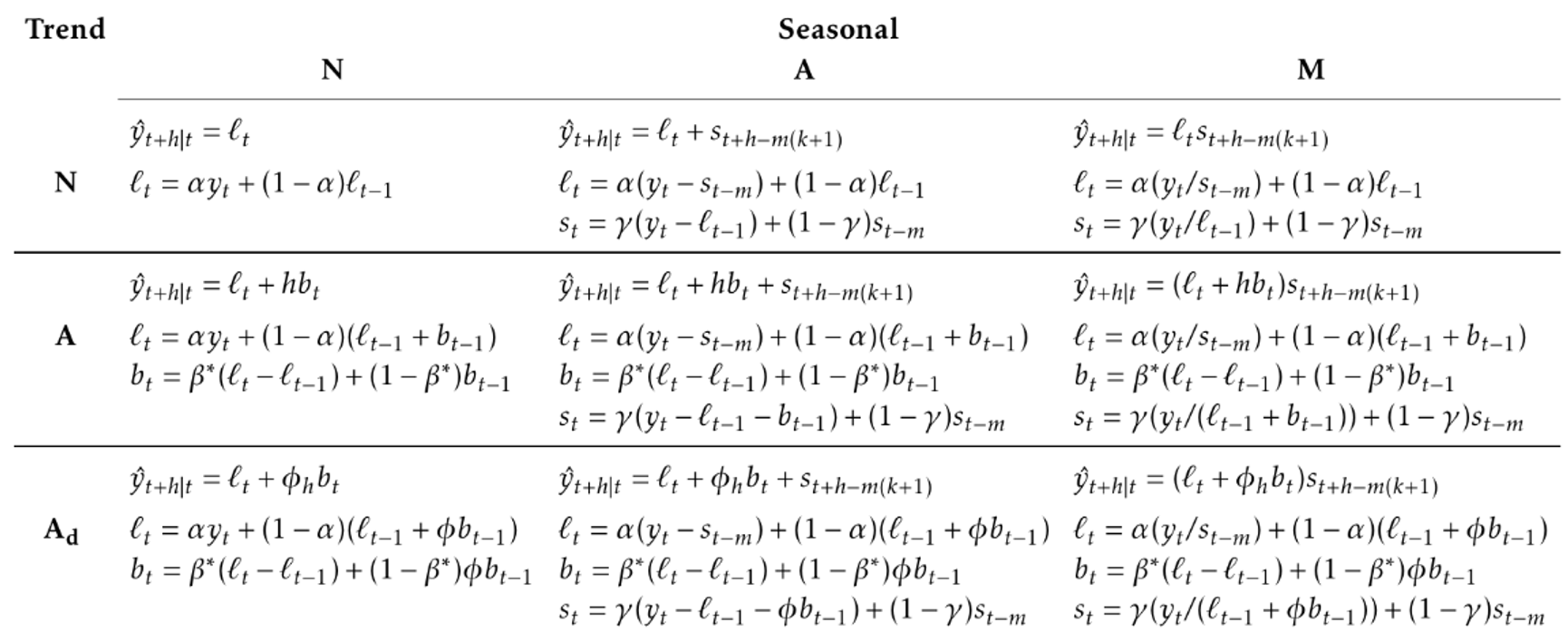

Exponential smoothing

Trend component - simple exponential smoothing (T)

The simplest exponential smoothing just models the trend as a weighted sum between the last prediction and the last observation

By recursive substitution, this becomes:

…which represents a weighted moving average of all past observations with the weights decreasing exponentially, which smooths the observations

There are various methods that fall into the exponential smoothing family. Each has the property that forecasts are weighted combinations of past observations, with recent observations given relatively more weight than older observations. All share the name “exponential smoothing,” reflecting the fact that the weights decrease exponentially as the observations age.

Equivalent representations

The component form gives the relations between the different model’s components. This is a procedural form, whose recursion gives the mean prediction. To pass from the component form to the state-space form, we must explicit the presence of measurement and process noise.

Component form

State Space form

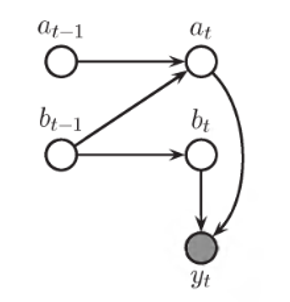

Holt’s linear trend method (T)

Holt (1957) extended simple exponential smoothing to allow the forecasting of data with a trend.

Component form

State Space form

where denotes the estimation of the level, represents the change of level (that is, the slope), always estimated with an exponential smoothing

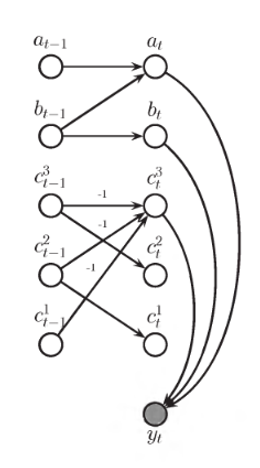

Holt’s Winters method

The Holt’s Winters method incorporates a single seasonality effect.

… and many more

Estimation

Unlike linear regression, no closed form → numerical optimization must be used.

Parameters are estimated maximising the likelihood.

For models with additive errors, equivalent to minimize the SSE

For models with multiplicative errors, not equivalent